Perhaps because of the proliferation of personal finance websites focusing on early retirement, I’ve noticed a lot of talk lately about safe withdrawal rates. I think this is absolutely terrific, as financial independence is one of the single most empowering life goals one can pursue! But greater exposure also has its downsides, as core assumptions such as the portfolio options, withdrawal method, and retirement length don’t always scale the way you might think and misconceptions can quickly propagate.

Withdrawal rates are an intellectual passion of mine, and I’m always looking for opportunities to contribute to the conversation. And with the recent boon in global portfolio data, I’m finally able to address one of the biggest questions that I’m starting to see more frequently these days.

Does the 4% rule apply outside of the United States?

It’s a very good question, as the Bengen and Trinity studies that established the 4% rule focused exclusively on the US market. And in my experience, there are actually two sides to this question even if one does not immediately realize it:

Is the numerical maximum SWR also 4% in other countries?

Does the portfolio assumption required to support that maximum withdrawal rate hold up in other countries?

You’ll usually see that second question swept aside in most withdrawal rate conversations, as numerous researchers have found (while arbitrarily limiting themselves to a single stock fund and bond fund) that about 80% stocks is the sweet spot for optimizing retirement portfolio outcomes in the US. Following that research, the advice to load up on stocks even in retirement is pretty much taken for granted.

So how does our basic US-centric understanding of safe withdrawal rates hold up in other countries? Are withdrawal rates truly universal, or are investors simply blowing a shiny American pinwheel while only assuming the numbers also work elsewhere? Let’s turn to the data.

First, let’s take the conventional wisdom at face value and look at the withdrawal rates a portfolio with 80% domestic stocks and 20% domestic intermediate bonds would have supported over the years. These numbers are calculated since 1970, do not account for fees, and look at a 40-year retirement period (more conservative than the traditional 30-year period found in most studies to compensate for the less conservative smaller data set — read this for more methodology info).

As you can see, the SWR for US investors was about half a percent higher than Canadian, German, and British investors experienced. And for Australian investors, only 2.5% would have been safe using the same methodology. Any smart Aussies responsibly following the same 4% rule based on solid US research could be in for a rude awakening!

Case closed? No way — it goes so much deeper than that. For a chaser, let’s compare these withdrawal rates to a much-maligned investor who ignored the stock market and simply invested their money in cash (local 3-month T-bills) for their entire retirement.

I bet you didn’t expect that!

Yes, Australians with their money in a treasury money market account were a full percent better off than their neighbors following typical retirement portfolio advice, and Canadians would have been in pretty much the same place with either choice. In fact, only in the USA and UK did loading up on stocks result in more than a 1% premium in SWRs.

You see, contrary to “common knowledge” seen through red, white, and blue glasses, high percentages of stocks are not always the best choice in every country. To explore that idea, check out how SWRs vary by percent stocks.

Now it’s starting to get really interesting. Only in the United States was the ideal percentage of stocks as high as 90%. In the UK it was about 70%, in Canada it was about 60%, and in Australia it was about 30%. And shockingly, in Germany not only was the ideal percentage of stocks as low as 10% but the resulting SWR was actually higher than the best one in the United States!

So is this simply a matter of some countries having superior stock and bond markets to others? Good question. To test that, let’s assume that everyone around the world has access to the same US stock and bond index funds that were used in the original studies that established the 4% rule.

While exclusively purchasing US funds does correct a few of the curves to favor stocks, it does not at all guarantee that the famed 4% rule established in the US applies to other countries. Only Canada provided similar SWRs, but only if investors ignored US-centric advice and held no more than 60% stocks. Withdrawal rates in different countries are complicated!

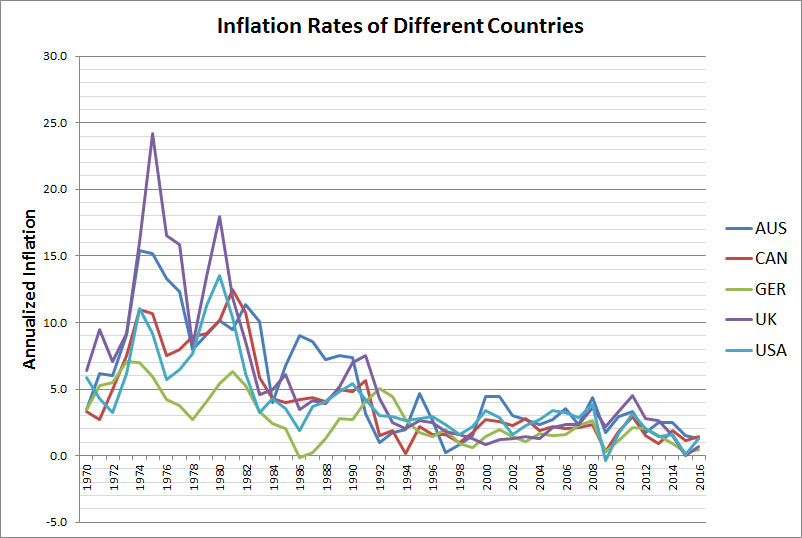

So if the funds are exactly the same, what is driving the difference in withdrawal rates? Two things: inflation, and exchange rates. Remember, withdrawal rate calculations are based on the assumption of maintaining constant purchasing power. Both inflation and exchange rates can greatly affect that, and they vary quite a bit by country and over time.

With inflation differences and exchange rate variations both affecting the results by double-digit percentages, it’s no wonder that simply buying US funds is insufficient to match US withdrawal rates for global investors. You can diversify your investments across assets and borders, but you can only live in one country at a time. And the inflation and currency in that home country matters a great deal to your financial security.

In fact, I would suggest that the data provides a good argument for investing (at least partially) in your home country. Not only will that bypass the effect of exchange rates, but it arguably also helps with inflation. Local stocks and bonds are not perfectly correlated to local inflation by any means, but local inflation is far more related to the local economy than to one halfway around the world. Completely detaching the engine of your returns from the inflation it needs to account for may have negative consequences for your portfolio that you did not anticipate.

So to recap, there are several reasons why the typical advice to invest mostly in stocks and withdraw an inflation-adjusted 4% does not automatically apply to investors outside of the United States. Every economy is different, so the performance of US markets may not apply to you. Portfolios with high percentages of stocks are not ideal in every country, so the recommended portfolios to achieve optimum withdrawal rates in the US may not apply to you. And if you invest internationally, differences in inflation and exchange rates alter the results even for the exact same fund so the advertised purchasing power of those returns may not apply to you. Basically, global investors should take all US-based withdrawal rate research with a huge grain of salt!

In addition, it’s also extremely important to remember that there’s so much more to investing than simply tweaking the percentages of a total stock market fund and an intermediate bond fund. If you think beyond those two arbitrary options, both the 4% number and the assumed preferred stock weighting are irrelevant from the start even in the United States!

So if the standard conclusions drawn from US-based retirement research are shortsighted even for many US investors and essentially useless for worldwide investors, what is a responsible prospective retiree to do? Just give up and hope for the best? Of course not!

Calculating the appropriate withdrawal rate for a particular portfolio in a specific country is pretty complicated business, but I’ve already done the legwork and am happy share my work. Simply visit the Withdrawal Rates calculator, and you’ll have access to all of my best data in a format designed for quick experimentation. And for information on how withdrawal methods also affect the returns be sure to also check out the Retirement Spending calculator. No matter your country and preferred portfolio, Portfolio Charts can help you understand how asset allocation affects your personal retirement plan.

Now I wouldn’t necessarily make a retirement portfolio decision based solely on the data here, and I encourage you to seek out as much input as you can find from contemporaries familiar with the nuances of your own market. Just because a concentrated bet worked well since 1970 (like investing in 100% Australian T-bills or even 100% US stocks) does not mean it’s the best idea today, but I’m happy to offer a fact-based reality check to back various retirement theories with real evidence and weed out the demonstrably bad ideas. Look for diverse portfolios that work well in all economic conditions, and you’ll be far better off than most people who simply fall back on the first easy answer they find.

Don’t simply depend on popular canned US-centric advice to plan your own retirement. Your decision requires the best data available for you — not for some hypothetical person with a different portfolio in a foreign country.

So get to it! Your future happily-retired self will thank you later.