With a nationally syndicated radio show, best-selling books, and a popular financial advice service, Dave Ramsey is one of the most famous names in the personal finance space. He’s so trusted that he’s also a mainstay in many churches as a guest lecturer preaching his own inspiring message of financial freedom. I’ve long admired his ability to help people work their way out of debt, and he’s doubtlessly touched more lives and improved them for the better than I can ever dream of reaching.

So as a fan of Ramsey’s message of self empowerment and snowball approach to debt elimination, I found it particularly painful to watch a recent episode where he goes on an extended rant about safe withdrawal rates. Long story short, he’s not only dangerously wrong but also angrily dismissive of an entire field of research on the topic. The reaction among financial types on social media has been equally swift and negative, with both professional investors and educated amateurs alike taking their own shots back.

Personally, I find the bickering on both sides to be mostly unhelpful because it distracts from the core issue — the truth. So for the benefit of Dave’s audience who just wants to properly understand the topic, I wanted to do something a little more constructive.

If you’re a Dave Ramsey fan who would like to understand why his advice is not the right way to approach retirement and how you can create a much safer plan, this article is for you.

Strong words for a simple question

For full context, the best place to start is to watch Ramsey’s discussion on safe withdrawal rates in his own words. Here’s the full clip with no editing that shows the entire segment.

For those who don’t have the time to listen to the whole 9 minutes, here’s my high-level synopsis including plenty of direct quotes.

A 30-year-old Ramsey fan calls in to talk about his desire for financial independence. He shares his net worth and wants to discuss how to best “turn that nest egg when I retire into income.” The caller cites research on Ramsey’s website which recommends a 4-5% withdrawal rate and another video by a Ramsey cohost George Kamel who recommends a withdrawal rate closer to 3%. He’s looking for guidance on which number makes the most sense for his situation.

The question appears to visibly anger Dave Ramsey, and rather than put words into his mouth I’ll just quote his own:

- “I don’t know what the hell George is talking about with a 3% withdrawal rate, because that’s completely wrong.”

- “The problem is that when you go down these stupid nerd rabbit holes in these Reddit threads with the morons who live in their mother’s basement with a calculator, then you put that out into the dadgum community and then people go ‘I don’t have enough money. It’s hopeless. I’ll never be able to save enough to retire.'”

- “So what you’re doing with this bogus math is you’re stealing people’s hope. That’s why I’m pissed about it. It’s hope-stealing with super nerds that have never really done anything to start with. They don’t have any investments, they just have theories. I’ve actually freaking got investments.”

- “There’s all these goobers out there who have always put this 4% crap in the market, and I’m just irate right now that we have joined the stupidity. It’s too low!”

- “The financial industry, with their moronic paralysis of the analysis pisses me off to no end.”

- “And what it sets up is this guy now, he doesn’t think he’s got enough money, and he’s already got 120 thousand dollars and he’s 30 years old and he’s on a plan to be very wealthy and he’s worried if he’s going to have enough money or not. Because stupid people put out low withdrawal rates.”

To give Dave credit, at least we know how he truly feels!

As you can imagine, even before you get to the substance of the argument that type of angry and dismissive approach set off quite the response among those who study these things for a living. Even as a bigger Ramsey fan than some others in the financial field, I’m always disappointed when someone I admire resorts to name calling over helpful explanations.

Dave Ramsey’s retirement math

Rather than linger on his insults and gross mischaracterizations, I think I’ll just embrace the “super nerd” label and focus on Ramsey’s own retirement recommendation. Here are the 3 key quotes that clearly characterize his thinking:

- “If you’re making 12 in good mutual funds, and the S&P has averaged 11.8, and if inflation for the last 80 years has averaged 4 percent, if you make 12 and leave 4 percent in there for inflation raises, that leaves you 8. So I’m perfectly comfortable drawing 8.”

- “The math I just gave you is the math. If you’re making 12 percent, and inflation is 4, and you leave 4 in there so your nest egg grows by 4, it’s simple. 8 is what’s left over.”

- “A million dollars should be able to create for you an eighty thousand dollar income, boys and girls, perpetually! Like forever! You should be able to pull eighty thousand forever, and never destroy it.”

To summarize, here’s Dave’s retirement math in a simple form that I’ll call the Ramsey equation:

Withdrawal Rate = Avg. Return – Avg. Inflation

The idea of feeling comfortable spending the average inflation-adjusted return admittedly does sound pretty reasonable on the surface, so I can understand why people might be attracted to the concept.

His advice in the real world

Before jumping to conclusions, I think it’s always fair to evaluate an investing recommendation with accurate historical data. So let’s give Dave the benefit of the doubt and model how his withdrawal plan performed for any real-world investors who dutifully followed his advice.

For the following analysis I’m going to use the Retirement Spending chart. Rather than looking at a single investing timeframe, it models every retirement start year from 1970 through today simultaneously and tracks the account values for every possible theoretical investor over time. That way, we can observe how every retirement scenario worked out.

For the portfolio input, I’m using 100% large cap blend US stocks to follow Dave’s specific mention of the S&P 500. Note that in the segment he cites an 11.8% nominal average for the S&P 500 as support for his 12% return expectation. To properly calibrate the comparison, I double-checked and verified that my data has an average of 11.7%. That’s really close, and the small difference likely due to the expense ratio that I also account for. Also, my inflation data has an average of exactly 4% which matches Dave’s number. So I believe it’s a fair portfolio to model perfectly in line with Dave Ramsey’s own data.

For the spending assumption, I used a $1mm portfolio with Ramsey’s recommended 8% withdrawal rate. Following standard withdrawal methodologies, that means that you take out $80k in the first year and adjust the withdrawal by inflation every year. The end result is that it maintains the same inflation-adjusted spending each year to support an identical standard of living, which also follows Ramsey’s expectations of withdrawing an inflation-adjusted $80k every year.

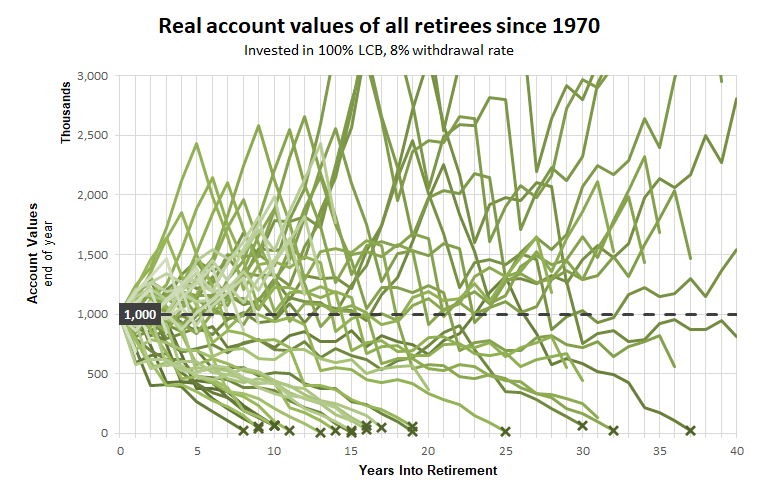

If you model every retirement start year since 1970 following those assumptions, track the portfolio values over time, and plot them all together, the final chart looks like this.

See the X’s at the bottom of the chart? Those are failures where the retiree completely ran out of money. Since it’s hard to see overlapping X’s, I checked under the hood and counted 21 failures out of 53 possible start years. Also, the “success” count includes recent start years that may also soon fail given a few more years of withdrawals.

So since 1970, about 2 out of every 5 retirees who followed Ramsey’s advice eventually went broke and even more may be on a doomed path. And the earliest failure happened just 8 years into retirement! For trusting investors expecting $80k forever, that’s more than just a rude awakening. It’s disastrous.

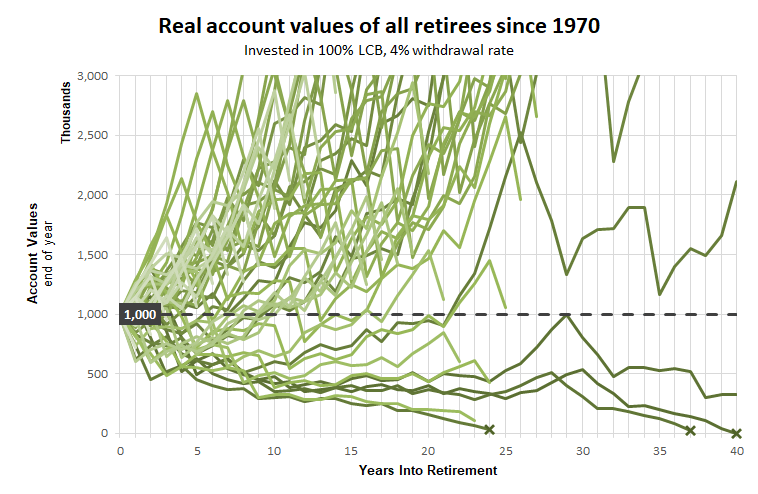

For comparison, here’s the same chart with a 4% withdrawal rate. See the difference? Yes, there are still failures. But they’re much less common and a lot further down the line.

While we’re here, one thing I find interesting about this chart is the crazy spread of outcomes. Even with the same initial account balance, portfolio, and conservative 4% withdrawal rate, many investors became fabulously wealthy while others still eventually ran out of money.

Some people argue that this is evidence that withdrawal rates can be increased in certain situations to spend down excess wealth while still protecting against the worst outcomes, and I think that’s definitely a conversation worth having. But the most important lesson in this context is about perspective. Whenever someone definitively cites their own lived experience as a reason you should just follow their same path without worry, how do you know they weren’t just one of the lucky investors who rode a hot market and never experienced true hardship?

So when Dave Ramsey pounds the table and proclaims that a retiree with a million dollars should be able to withdraw 80 thousand dollars a year “forever”, a simple sanity check shows that it’s clearly not true in a shockingly large number of cases. That’s why so many responsible financial advisers are up in arms about his advice. While I respect Dave for helping so many families dig their way out of debt, real people with good hearts and trusting mindsets can get seriously hurt by extending their faith to his flawed retirement advice.

The problem with averages

While it may seem crazy that a popular financial voice can get something like this so wrong, it’s actually a lot more common than you think. People just aren’t naturally wired to understand uncertainty, which is why they tend to lean so heavily on averages.

As an example, I’d like to share one more Dave Ramsey quote that may help frame the problem:

“If you think you can only pull of 4 percent off of investments making 12, where the flip is the other 8 percent going?”

Dave Ramsey

Now we’re getting somewhere, as that is actually a very good question! Here’s my best explanation of how that all works.

Look again at the Ramsey equation:

Withdrawal Rate = Avg. Return – Avg. Inflation

The primary issue with this approach is the important qualifier that is included without any context — “Average”. If investors received exactly 12% nominal every year with exactly 4% inflation, then Ramsey would be absolutely correct. But have you checked your investment balance in the last few years or looked at the price of groceries lately? Constant numbers are not at all how actual markets work.

When it comes to real-world performance, the most important thing to remember is nobody receives the average. Once you introduce the variability of returns into the equation, things get a lot more complicated. Some people earn more than that on their own investing timelines, and some much less. And when it comes to protecting your hard-earned life savings in different market conditions, that’s why it’s absolutely critical to look at the full range of outcomes.

To illustrate this, here’s a Target Accuracy chart for the same large cap blend portfolio. It has the same ~12% average return and 4% average inflation that Ramsey cites. Pay attention to both the straight gray line and the blue and red extremes.

The gray line tracks the average return as if it was a constant that repeated every year, and it is straight like a laser because the Y-axis uses what’s called a log scale that shows equal percentage changes as equidistant. That perfectly predictable growth is what people imagine when they hear about a 8% average real return, and is what Dave implies with his explanation.

But think about it — when is the last time that you received the exact same investment return on a stock every single year? Never? Well, you’re not alone! Because investments don’t work like that, and they go up and down all the time. In this image, the blue lines show the outcomes of lucky investors who beat the average and the red lines show the outcomes of unlucky investors who trailed the average.

Now, look at the bottom 10-year investing sample. Ramsey cites the 10-year average in his explanation, but you may be surprised to learn that the spread in outcomes over 10 years was nearly $4 million. Check out the worst-case outcome where not only did the portfolio not grow but it even shrank by more than 30%. And that’s without withdrawals!

Finally, multiply an $80k a year withdrawal by 10 years and subtract it from those bottom numbers. Even if the average is still doing fine, the unfortunate soul with a bad sequence of returns is now broke and the 15th percentile baseline is in really bad shape. And while you’re at it, think about how taking $80k out of a portfolio that started at $1mm but shrunk to $675k in the middle of a slump is no longer just an 8% withdrawal but 12% of the remining balance. That’s how retirement drawdowns can quickly spiral in down markets and why volatility can’t be ignored.

So yes, the average investor was fine. But like proudly aiming a nerf gun with a laser pointer, the real world is messy and there’s an excellent chance your own investing timeframe will not be average. When applying the conclusions to a retirement where there’s no guarantee of ever making that money back, thinking beyond the average experience to the less-rosy scenarios is a critical step to making wise decisions.

That process of evaluating investing performance and identifying withdrawal rates that are not only useful on average but also safe for everyone is exactly what famous and highly respected researchers like William Bengen, Wade Pfau, the team with the Trinity Study, and many more have spent years talking about. By the way, for more information on why depending on averages in withdrawal rate discussions just doesn’t work, I highly recommend Bengen’s original paper on the topic: Determining Withdrawal Rates Using Historical Data. It’s an easy read and explains it better than I ever could.

Building on the same research methodologies with my own data skills, here’s a Withdrawal Rates chart for the 100% large cap blend portfolio. This shows how withdrawal rates vary over retirement year and duration. Every blue line is a real-world retirement scenario since 1970, and the orange line tracks the worst case.

See that orange dot? That’s the worst-case outcome over any 30 year retirement. It’s called the safe withdrawal rate, and it’s where the famous 4% rule comes from. And see the green dot? Instead of depleting the portfolio to zero in the worst case, that’s the withdrawal rate that maintained its original $1mm inflation-adjusted principal. It’s called the perpetual withdrawal rate, and there’s a good chance it’s where Dave Ramsey’s caller got the 3% number he was asking about.

So swinging back to the (well-informed) caller that kicked this all off, here’s how I’d answer his question: For a standard stock/bond portfolio, 4% is a good guideline to last 30 years while 3% is a better choice to plan for if you succeed in your financial independence goal and retire well before 65. No withdrawal rate is foolproof, but it’s a solid speed limit to help you stay on the road and out of the ditch.

And to answer Ramsey’s question on where the extra 8% went, I’d say that half of it went to inflation and the rest was an illusion that arose from failing to consider that investing returns are never constant. It’s all based on transparent math and solid research for those willing to seek it out. But to truly understand it, you’ll have to think beyond averages and embrace the reality that uncertainty is an important factor in wise risk management.

Where Dave has a point

Contrary to some others who may fill your timeline with snark, I’m not the type to enjoy a takedown article. Yes, I think Dave Ramsey is provably wrong about withdrawal rates to the point where I feel compelled to properly explain them to protect people from harm. But I have no malice towards Dave, and if he reads this I hope that comes across. We both just want to see normal people live happier lives thanks to productive financial choices.

So to balance the negatives, I’d like to close with two areas on this topic where I think Dave makes a good point.

First, while I absolutely do NOT agree with his derisive dismissal of the smart retirement researchers who work in this area, I do understand where he’s coming from in some of his frustration. As someone who has read way more than the average amount of retirement commentary, I actually share some of his angst with people who push limited research conclusions as scientific laws of nature.

For example, more people promoting withdrawal rate research than I’d like to count lean heavily on myopic assumptions such as severely limited asset options, single-country coverage, or unrealistic methodologies. And as a result, it’s strangely controversial in some circles simply to point out that the 4% rule calculated for a mix of very specific US stocks and bonds does not apply to every portfolio. In some cases it really is too low, and in others even 4% can be risky.

So instead of just throwing stones, I’d encourage others to take some time to read some of my work on retirement investing. From calculating the safe and perpetual withdrawal rates for any combination of assets in a dozen different countries to studying the effect of variable spending strategies on retirement performance, I’ve got you covered with more data than you probably even know exists. It’s a lot more interesting than just arguing over 4 versus 8 percent.

And second, one part of Dave’s answer that I find genuinely compelling is his repeated desire to give investors hope. While I disagree with his solution of promoting unrealistically high withdrawal rates, I get where he’s coming from. Just like prioritizing paying off small debts over those with high interest rates in his debt snowball isn’t about making the financially optimal move but the emotionally motivational one, hope also matters in retirement. But I believe it is best inspired by example, not by dismissing the truth and insulting others who share it.

So here is my message of retirement hope.

Choose empowerment

Yes, financial independence is an achievable goal. It’s not easy, and it will take a lot of hard work, perseverance, and something closer to a 4% withdrawal rate than 8% if you’re being smart about risk. But don’t let those numbers steal your hope! Instead, realize that their true purpose is to give you confidence.

Perhaps you’re not aware, but Portfolio Charts was actually born of the extra free time that financial freedom enabled. In fact, you’re reading this today because smart people like Bob Clyatt were willing to lay the numerical groundwork that allowed me to make major life changes without fear. The thing is, you don’t get that level of confidence from simple averages and silly rules of thumb. One important lesson I learned from engineering is that true faith requires thorough tests that push ideas to their limits.

I’ve personally spent countless hours researching retirement and sharing everything I know, and I do all of this largely to pay it forward to the next generation of people similarly seeking a way out of the rat race. And no matter your age, that generation includes you. I did it. And you can, too.

So for the many Dave Ramsey fans out there who have benefitted greatly from his spending and saving advice, I’m sure you’re thrilled with the results. Escaping debt is amazing! When you reach the point of taking the next step towards building a portfolio to fund your retirement, I simply suggest that you branch out and read more on the topic from others whose specialty is in that area.

I’d be remiss if I didn’t recommend reading about the many excellent portfolios here, and I’d love if you’d do me a favor and share this article with other Ramsey fans that you think can benefit from its message. But I also don’t claim to have all of the answers, and there are many great voices out there.

So seek them out! And never be afraid to ask hard questions. The path of personal growth from blindly following advice to truly understanding the tradeoffs and making your own informed choices is an important part of the journey.

Choose empowerment, and freedom will follow. You’ve got this.

Join the conversation

![]()